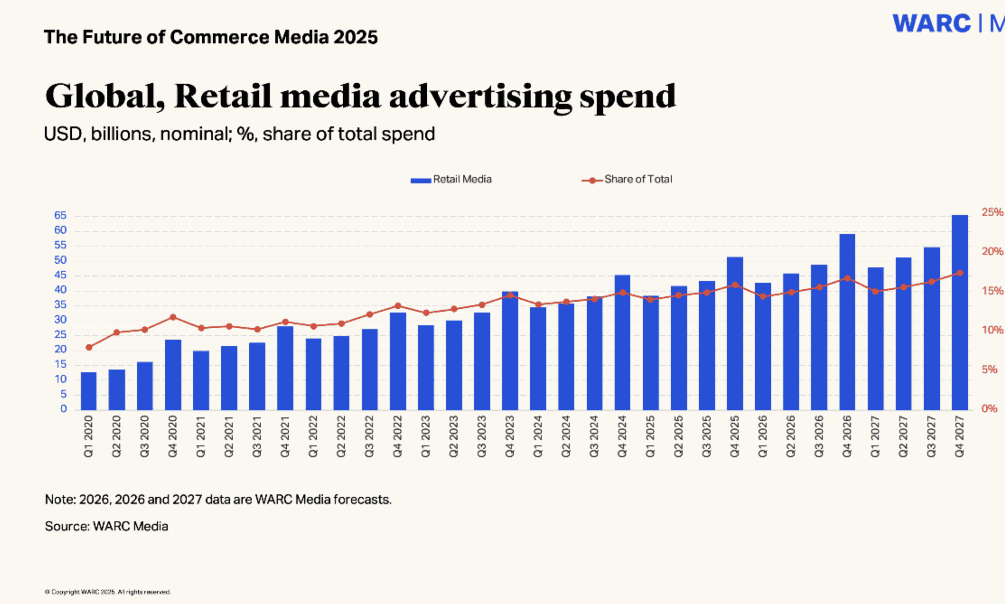

The global retail media ad market continues to grow, with figures from analysts at WARC predicting that it will surpass $200bn by 2027. However, it is a rapidly evolving industry and, while growth remains strong globally, its rate of growth is starting to slow – recalibrated by attention moving away from sponsored search and into a raft of other channels.

The rise of social, off-site and CTV tie-ups is seeing brand spend become more granulated and is forcing retailers to rethink what their retail media offerings actually comprise.

It is not news that this means retailers running RMNs must now adapt from being media sellers into media platforms. However, where it gets complicated is in how they do this through an increasingly fragmented array of channels and against a backdrop of massive industry consolidation, where a few key commerce media players dominate.

This can be seen in the figures. According to the latest WARC Media forecast, worldwide investment with retail media networks (RMNs) is set to reach $174.9bn this year, up 13.7% year-on-year, before rising a further 12.4% in 2026 to reach $196.7bn, representing 16% of all ad spend. However, topline growth rates are steadily slowing towards single-digit levels – from 38.6% in 2021 to a forecast growth rate of 11.6% in 2027.

While this slowing make look alarming, it is worth noting that it significantly outpaces the total digital ad market – forecast at 7.9% in 2025 – and traditional advertising formats like TV. However, it does point to how a rapid shift is occurring within the sector.

What this means for RMNs

What appears to be happening is that brands are now much more savvy about what they are looking for from retail media marketing. They are spoiled for choice and playing in a hugely competitive, buyer’s market.

As a result, brands are shifting focus from solely on-site, lower-funnel sponsored search – which is where this slowdown in growth is most prominent – to off-site display and full-funnel solutions, including CTV and social media integrations to find new avenues for expansion.

According to James McDonald, Director of Data, Intelligence & Forecasting, WARC: “Display advertising currently represents less than 30% of total on-site retail media spend, however, this balance is poised to shift as retail media becomes more integrated with brand digital budgets. Much may depend on the adoption of agentic AI, which threatens the high human traffic volumes that have monetised the retail media networks to date.”

Industry consolidation

While Agentic AI is going to have a huge impact on retail media, as discussed here, a more pressing concern for retailers running RMNs or looking to set them up is the rapid consolidation within the industry – a consolidation that is almost as rapid as the deceleration of growth in RMN ad spend – and how that itself is leading to a rise in the power of dominant players such as Amazon.

Combined with the entry into the market of ‘commerce media’ players that lie outside or on the fringes of traditional retail and suddenly the retail media market looks a daunting prospect.

Consolidation is occurring as the market (rapidly) matures and, as we have seen in the WARC figures, brands are becoming more selective with their ad spend, concentrating budgets on fewer, more established RMNs.

This leads to an over dominance of major players, with giants like Amazon and Walmart dominating the market – with just these two expected to account for over 84% of all retail media ad spending in the US in 2025. Their scale and robust first-party data give them a competitive advantage.

This puts increasing pressure on smaller RMNs. These retailers often lack the necessary digital footprint or resources to generate meaningful ad revenue and face pressure to build out their capabilities or partner with third-party tech providers – itself a trend seen across retail media and well documented in RetailX’s Offsite data workbench report.

There is also a change in tack among brands internally. There is a growing move toward breaking down silos and merging traditional shopper marketing, trade and digital media teams and budgets into a single, cohesive retail media strategy, further streamlining where money is spent.

In essence, the retail media market is evolving from an “explosive growth” phase to a more mature and strategically focused one, where scale and robust, measurable offerings are determining the long-term viability of RMNs.

Is broader commerce media the answer?

Partly as a result of all this, broader ‘commerce media’ is emerging as a full-funnel solution for many brands, with more ad formats and channels to complement granular first-party data.

A recent survey by ad-tech company Infillion found that two in five (40%) of agency-side executives who buy retail media see it as a full-funnel solution, while another 7% agreed it is an upper-funnel opportunity.

But new strategies and definitions of success will be needed to help this channel escape from a tight focus on narrow, lower-funnel conversion and from relying on siloed metrics like ROAS.

Infillion too suggest that there are a growing number of retail media channels and ad formats that can support truly full-funnel strategies. It also champions CTV, off-site, digital out-of-home and in-store advertising, as these can enable brands to execute full-funnel strategies that bridge digital and physical shopping experiences. And many commerce media players are already encroaching on this – not least Amazon.

Amazon aspires to dominate open web advertising

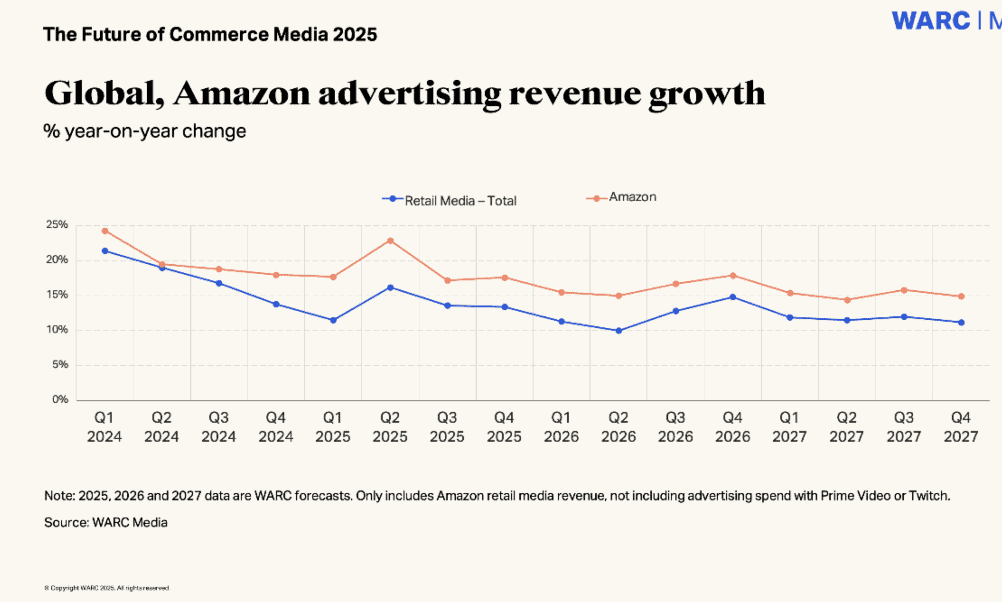

Amazon, the world’s largest commerce media seller, continues to dominate the commerce media landscape, maintaining 15% year-on-year growth, according to the WARC data, through its full-funnel expansion and strategic demand-side-platform (DSP) partnerships.

Inventory partners now include TV streaming platform Roku, enabling advertisers to reach an estimated 80 million US connected TV households alongside big hitters such as Disney, Netflix, Spotify and Microsoft. Amazon claims its ad-supported monthly reach in the US has tipped over 300 million, while eight in 10 UK households can be reached with Amazon DSP.

In fact, research by Skai found that more than 20% of all ad investment with Amazon is now allocated to its demand-side-platform (DSP) – double the share recorded two years ago – as advertisers look for greater efficiency.

For retailers this means retail media is no longer just about having shopper data, but about turning that data into programmatic, cross-channel targeting capabilities. To do this, many that lack the scale of Amazon, Walmart, or Tesco will have to now focus on building media ecosystems that advertisers can plug into easily and will need to operate with the same sophistication as traditional ad networks. In short, it is no longer a truism, but a fact: retailers really must evolve from media sellers to media platforms and they must start now.