Almost all retailers are talking about transformation in their business, but their approaches are alarmingly inconsistent: multichannel, omnichannel, data-driven, mobile-first, digitally-led, customer-centric, and more. In many cases it’s just a veneer –transformation on the outside –but scratch beneath the surface and not much has changed. The reality of managing a truly customer-centric business has to cut deep into the entire organisation. At the heart of it should be a new customer-centric operating model. In the past, retail decisions were aligned to stores and products. Customers were obviously important, but stores were a proxy –an aggregation of local customers. Store like-for-likes were a good measure of overall performance and customer relevancy. Customer actions were left to the CRM team, if one existed, and mostly consisted of broadcasting promotions.

Today, digitally-enabled consumers have changed the fundamental economics and dynamics of retail – consumers have been unshackled from the geography of stores. As the share of online penetration and influence has increased, online cannot be regarded as ‘just another store.’ The new reality becomes clear when retailers reach the tipping point of having negative like-for-likes but increasing overall revenue: the traditional “four walls” view of retail performance no longer works. Retailers need to pivot their focus from stores to customers.

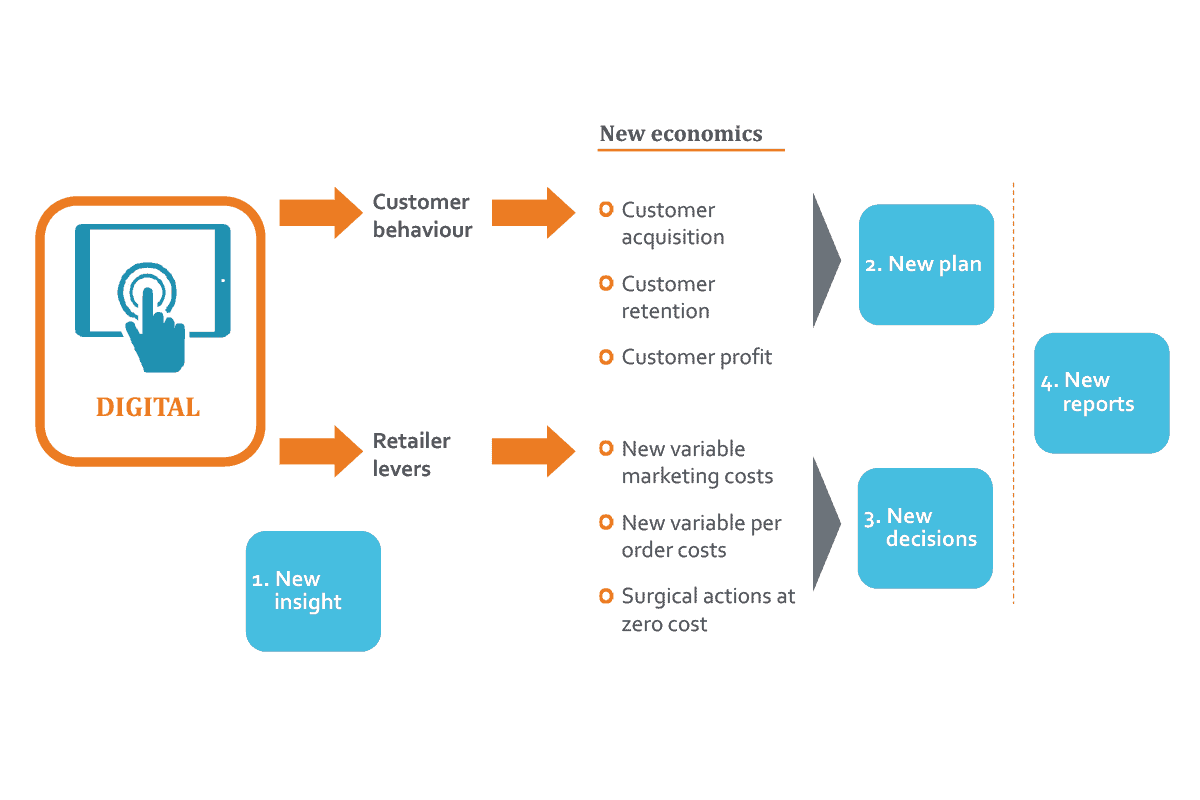

Almost everything is different in the customer-centric, data-rich, digitally-driven retail world:New revenue drivers (customer acquisition and retention); New variable marketing costs (cost per click, visit, transaction); New variable per-order costs (picking, packing, packaging, delivery, returns); New digital levers that allow retailers to take surgical actions (at customer, SKU, session level).

THE FOUR PILLARS OF CHANGE

It is the combination of these dynamics that requires retailers to change their approach to insight, planning, trading and reporting.

1. New Insights on Customers

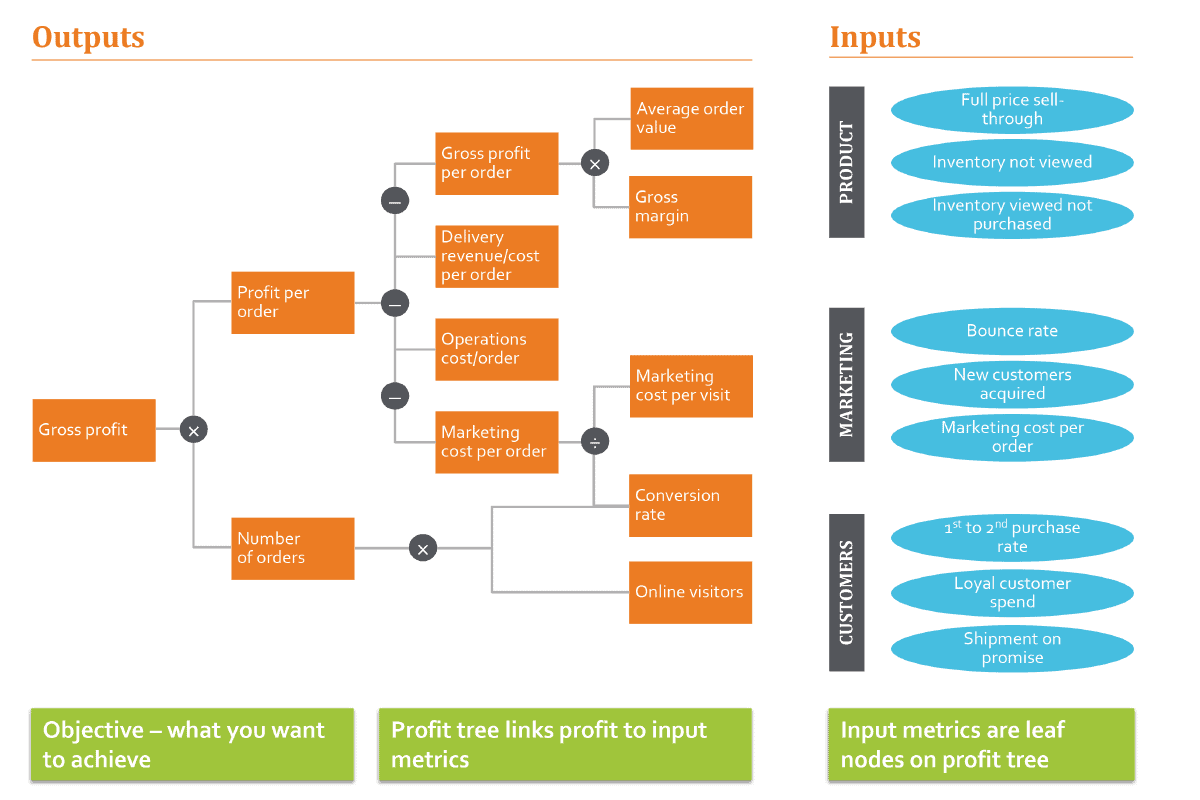

Retailers have always used the drivers of the P&L to understand their business – traditionally by geography, store, category, brand or store format, with actions aligned to these same drivers. Retailers now have data at a customer level, can understand customer profit and can take action at a customer level. Customers are not equal – some matter more than others – and it is crucial for retailers to understand the profit and potential profit of every customer. A customer decile analysis brings this into sharp focus and highlights the fact that most retailers are actually running two very different businesses – the average customer does not exist: The top 5-10% of loyal customers who will typically make up 50% of revenue and 80% of profit. They shop regularly, pay full price and are brand loyal; A long tail of transactional customers.

CUSTOMER DECILE ANALYSIS

To be truly customer centric, you need to imagine a customer P&L – for every customer, know what are the actions that will drive incremental profit and what is the ROI for different types of actions. What are the characteristics of high and low value customers? Which products and brands acquire and retain high value customers? What marketing acquires and retains high value customers? Who are the low value but high potential value customers? What actions drive incremental customer LTV? It is also critical to make sense of the “digital exhaust” – the torrent of data from an individual customer’s browsing, searches, product views, basket adds, email clicks and marketing exposure. This data is vital to understand the customer’s intent and engagement to ensure that CRM actions are personalised, and retention investments are commensurate with the customer’s churn risk and potential value.

A Lesson from Amazon

Amazon has mapped each stage of the customer’s journey to understand the incremental lifetime value (LTV) of each step – for example: making the first purchase, making a purchase in a new category, signing up for Prime, buying an Alexa device, browsing a new category, buying a Kindle… Amazon has modelled the incremental LTV for each of these High Value Actions (HVAs), which is effectively a “common currency” for managing a customer-centric business. This approach allows every decision and action to be overlaid with the customer LTV lens.

- New Customer-Centric Plans

It is fundamental for retailers to set an achievable business plan. In the past, retailers’ growth was driven by simple math: same-store sales growth and new stores. However, many retailers are now going wrong because they set an overly ambitious revenue trajectory, buy inventory to this plan, then find themselves behind plan and overstocked. They run promotions to get back on track, which not only kills margins, but also trains customers to expect discounts.

THE RETAIL SPIRAL TO AVOID

The key to success is to build a customer-centric business plan:

- Project revenue from the existing customer base.

- Determine the number and type of new customers required to hit plan.

- Triangulate with category, channel and marketing plans.

At the core of this new model is an explicit growth vs. profit trade-off: accelerating customer acquisition can reduce profits in the short term but drive long-term growth; alternately, dialling down customer acquisition will have the opposite effect. There is no right answer, but smart retailers are clear about whether they are trying to drive cash, medium-term profit or long-term growth and can then adjust their path accordingly. Too many retailers make the mistakes of benchmarking growth rates against retail like-for-likes, creating unrealistic top-down targets, extrapolating from historical rates or focusing too much on top-line sales. Once the overall objective is set, retailers need to set plans for categories, channels and marketing based on customer outcomes:

- Marketing: allocate marketing spend across the various marketing touch points to optimise customer acquisition and retention.

- Channel: set customer acquisition and retention targets by store, and for online.

- Product: build range based on the products/brands/categories aligned with customer acquisition and retention. Allocate range and size ratios to stores based on local customer characteristics.

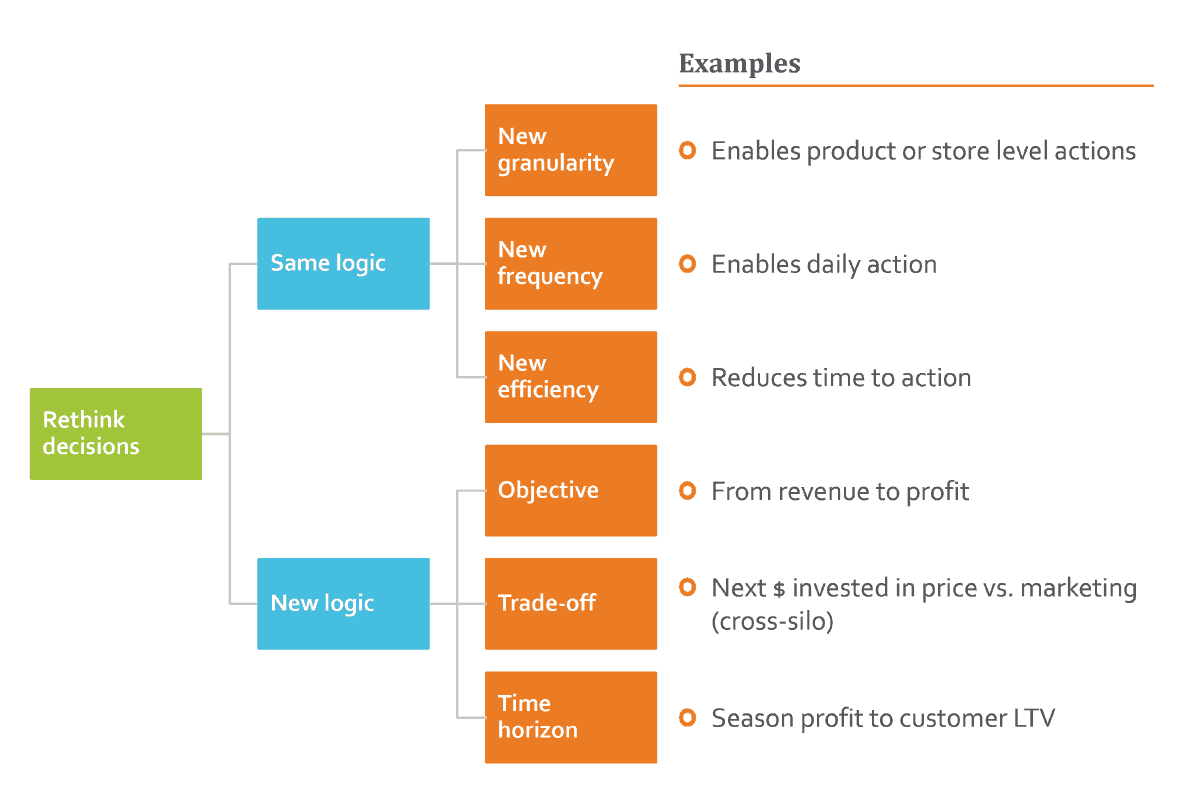

- New Trading Decisions

Retailers’ actions are typically blunt, based on sparse data and reliant on physical execution, and predominantly taken at the aggregate level of stores, categories or customer segments. Thirty years ago, the advent of computers gave retailers the abilityto rethink processes, but success required processes to be reengineered – if retailers simply computerised their existing processes they missed the opportunity. Now new technologies are giving businesses the ability to rethink decisions.

Some decisions will remain the same, but digital levers can be used to transform their efficiency, frequency or specificity. For example:

- Decisions that have required data manipulation in spreadsheets can now be completely automated.

- Decisions that have historically been taken weekly (in a trading meeting) can now happen every day, or every hour.

- Decisions that have historically been taken at category-level can now be taken (and executed) at product or even SKU-level.

But many trading decisions will need to be completely rethought with a different logic. For example, if a product is overstocked, retailers now need to decide whether to increase its exposure (more marketing), trigger a customer-specific promotion or offer a price discount? More generally, retailers now need to review their core trading decisions through the lens of customer profitability.

- Marketing: do we optimise to session profit vs. customer LTV?

- Channel: do we make decisions based on four walls profit vs. customer profit in store catchment area?

- Product: do we focus on season profit vs. customer acquisition?

HOW TO RETHINK DECISIONS

- New Customer-Centric Metrics and Reporting

Retailers’ reporting has traditionally focussed on aggregated averaged outcomes– e.g., like-for-likes, sell-through, inventory turns – that are used to tell a simple story. A clear picture emerges of performance across stores, across categories, across buyers and across managers. The metrics are mature and benchmarks are plentiful and meaningful. This made sense in a world where the aggregated data (e.g., at store or category level) aligned with the frequency and specificity of the decision being made. Moreover, the aggregation of data in physical retail has a naturally homogenizing effect that makes the averages helpful. The changes described above now require a different approach given:

- Focus on profit – reports need to be decomposed to understand the drivers of profit. It’s easy to drive revenue and depress profit in the customer-centric world.

- Faster and more specific reporting – reports need to align to the frequency of action, and need to make sense of millions of customers, and customer-centric actions. The key here is to measure inputs as well as outcomes.

- More granular – digital data provides incredible detail on every customer impression, click, visit and transaction, which requires reports to be deaveraged to understand what’s driving performance.

Unlike physical retail, aggregatedaverages are the enemy of the customer-centric retailer– they are generally unhelpful, often misleading and rarely representative. Retailers need to review their core trading reports and metrics to ensure that:

- Things are measured that matter to customers and drive action [what Amazon calls “controllable input metrics”]. A good example is page-weighted availability for high value customers – are you in-stock with the products that high value customers are looking at?

- Reports focus on outliers and anomalies– it’s critical to highlight waste and inefficiency to understand what can be improved. For example, how much money are you spending on digital marketing for products that are sold out?

- Metrics are deaveraged– by store, by SKU, by customer – to understand the right level at which to take action. For example, how often are you taking a product-level action when the issue is at SKU level?

NEW APPROACH TO REPORTING

Retailers no longer have the luxury of being unwilling or unable to change. Anyone who takes this transformation seriously will recognise just how sweeping and profound these shifts have to cut into their organisation. Enabling the new insights, new plans, new decisions and new metrics needed to create a new customer-centric operating model cannot be accomplished through minor superficial tweaks.

To truly make customers the focus of the business requires enabled senior leadership, such as a Chief Customer Officer, who can cut across silos and channels with the bigger picture in mind. Navigating with AI and data science at the heart of the organisation, managers need to have the skills and understanding in AI that then allow them to successfully achieve the necessary balance between human and AI algorithm-based decision making. Mistakes and bumps in the road are inevitable. Transformation is a significant challenge, not to be underestimated. It is imperative to create a culture where these bumps are seen as opportunities to learn and transform in order to foster growth. A skilled, nimble leadership and culture, as well as an employee base empowered by technology, are the vital elements to embarking on a journey of innovation and ultimately a successful (and profitable) future.