The 2026 FIFA men’s World Cup will be the biggest in the tournament’s history, hosted across Canada, Mexico and the United States and featuring more matches than ever before. Yet, despite large audiences, rising rights fees and expanding sponsorship packages, the World Cup’s measurable contribution to ad growth appears to be weakening – but that may well be an opportunity for retail media.

While the World Cup is expected to inject $10.5bn into the ad market, according to the latest data from WARC Media’s forecast, advertisers are no longer competing within a single commercial surface, but are having to engage with fans across diverse touchpoints beyond traditional broadcast rights.

Alex Brownsell, Head of Content, WARC Media, says: “This World Cup is no longer just about live matches — brands will engage with fans across touchpoints before, during and after matches have concluded. Media plans will include platforms that benefit from the conversation about the World Cup without the burden of bidding for rights; from creator content to podcasts, turning conversations around the games into powerful opportunities for connection and impact.”

This also presents an opportunity for retail media, with retailers seeking to capitalise on these pre-, during and post-match opportunities in more targeted ways.

Diminished advertising impact

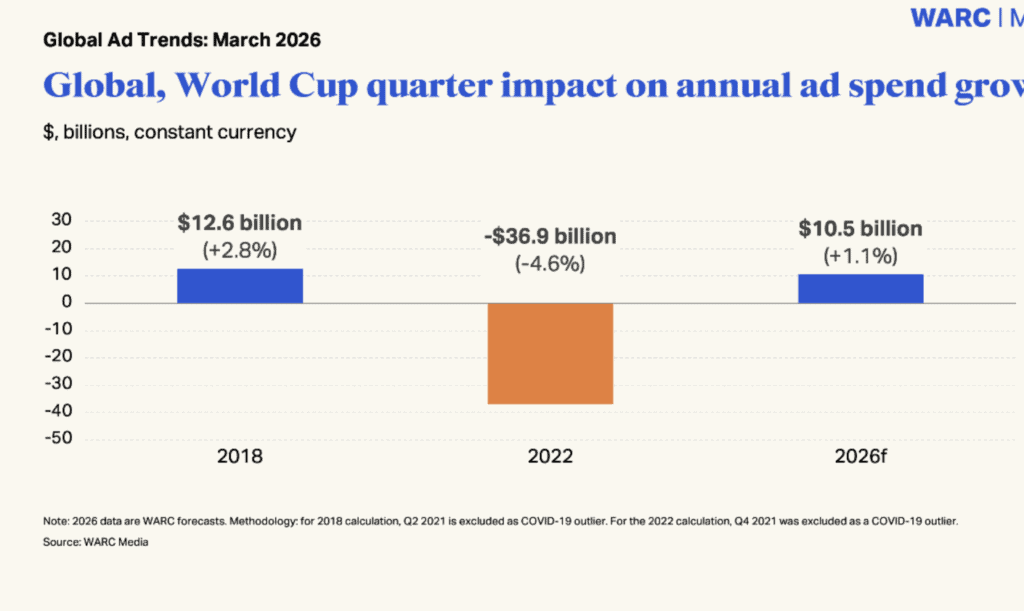

The 2026 FIFA World Cup promises record-breaking global audiences and a $40.9 billion boost to global GDP, yet its direct impact on ad spend growth is diminishing. WARC Media forecasts show a modest $10.5 billion uplift into the global ad market during the quarter the event takes place, marking a 1.1% incremental gain versus the Qatar World Cup in 2022. In contrast, the 2018 World Cup in Russia drove a $12.6bn (+2.8%) ad market boost.

Annual advertising spend growth during World Cup years is inconsistent, driven more by broader economic cycles than tournament cycles. Even for host markets, the tournament does not guarantee market-level acceleration or outperformance.

In the US – where soccer competes with popular domestic sports – the World Cup’s effect on ad investment is modest and inconsistent. In most positive years, the impact has been between 0.4-1% of total ad spend. Annual ad spend for Mexico, and a similar pattern is visible in Canada, shows no consistent pattern of acceleration in World Cup years. WARC Media’s forecast of approximately +4% for Mexico, is positive, but not exceptional for a host market.

Shifting audience consumption

Linear TV audiences are increasingly in decline as multiplatform consumption rises with expanded digital viewing. Qatar 2022 reached 2.87 billion people for at least one minute, yet linear reach fell 11.9% versus 2018. Multiplatform consumption rose as digital viewing expanded, particularly in China and India.

Audience fragmentation will be further highlighted during this upcoming tournament as attention shifts beyond the games to the conversations around games. TikTok has become a FIFA partner, and will show behind-the-scenes footage and YouTube, also a preferred platform, will stream live matches from media partners.

CTV is also getting in on the action with platforms such as Netflix looking to monetise the conversation around the games through video podcasts.

While tournaments drive TV and OOH revenue, premium pricing often displaces regular advertisers, with gains reflecting spend redistribution rather than market expansion.

Retail media impact

Retail media will play a critical and somewhat counter-cyclical role in the 2026 FIFA World Cup, particularly as the tournament’s ability to drive incremental ad growth weakens and spend becomes more distributed across channels. Rather than competing directly with high-cost broadcast inventory, retail media networks (RMNs) are uniquely positioned to capture performance-driven budgets that activate around moments of heightened consumer intent before, during and after matches.

Globally, the World Cup is expected to accelerate retail media revenue growth, but not through a step-change uplift in total ad spend. Instead, growth will come from reallocation. As brands face inflated prices for traditional media and fragmented audiences, many will divert budgets into retail media environments where spend is more measurable and closer to purchase. This is especially relevant as World Cup campaigns increasingly aim to convert cultural attention into immediate sales — something retail media is structurally designed to do.

Retail media will see the strongest activation in the pre- and post-match windows, where consumer behaviours such as grocery shopping, alcohol purchases, electronics upgrades and apparel buying spike. Sponsored product listings, onsite display, and offsite retail media (via CTV, social and programmatic extensions) will allow brands to align with match-related demand signals without needing official sponsorship rights. During live matches, while retail media is less central, second-screen behaviours — such as mobile browsing and in-app shopping — will create complementary opportunities.

Regionally, the impact will vary:

- North America (US, Canada, Mexico): As host markets, retail media will benefit from increased commerce activity tied to viewing occasions (e.g. food delivery, home entertainment, merchandise). However, similar to broader ad spend trends, the uplift will be moderate rather than transformational. The US in particular will see retail media absorb budgets that might otherwise have gone to linear TV, driven by its advanced RMN ecosystem such as Walmart Connect and Amazon Ads. Growth will likely outpace total ad market growth, reinforcing retail media’s share gains.

- Europe: Time zone challenges will dampen live viewing, shifting engagement to highlights, social content and next-day consumption. This dynamic favours retail media, as advertisers prioritise always-on, performance-led channels over costly live slots. Grocery and convenience-led RMNs will benefit from match-adjacent purchasing, though overall revenue uplift will be incremental rather than event-driven.

- China, India and the wider Asia-Pacific region: With many matches airing outside peak hours, retail media will play a key role in capturing deferred engagement. E-commerce-led ecosystems such as Alibaba and Flipkart will integrate World Cup-themed promotions, leveraging retail media to monetise traffic driven by digital content consumption rather than live viewing. Growth here will be tied to broader e-commerce expansion rather than the tournament alone.

- Latin America and MENA: These regions, which show the highest levels of football engagement, present the strongest relative opportunity. Retail media usage is less mature but rapidly growing, and the World Cup will act as a catalyst for increased advertiser adoption. Brands will use RMNs to tap into heightened fan enthusiasm and frequent shopping cycles, particularly in grocery and mobile-first environments.

In terms of usage, the tournament will reinforce three key trends in retail media globally:

- Integration into full-funnel planning, as brands link upper-funnel World Cup moments with lower-funnel conversion tactics.

- Expansion of offsite retail media, particularly into CTV and social environments tied to football content.

- Increased demand for real-time activation, with retailers leveraging live signals such as scores, match outcomes, player moments to dynamically optimise campaigns.

Overall, while the World Cup’s direct impact on total ad market growth may be diminishing, its role as a catalyst for how budgets are deployed is significant. Retail media sits at the centre of this shift – not as a beneficiary of incremental spend, but as a key destination for redistributed investment in an increasingly fragmented and performance-driven media landscape.