Retail media is already established as a high-margin income stream that can meaningfully offset the low margins of traditional retail. However, this stream can be scaled even further through digital marketplaces. In Part 2, Colin Lewis examines how retailers use marketplaces to supercharge their retail media business. Read Part 1 here.

Marketplaces are now one of the most significant components of global ecommerce, with the largest platforms becoming household names. For retailers, three key questions remain:

- Should they tap into the digital marketplace opportunity?

- Can it accelerate other monetisation opportunities, such as retail media?

- Which retailers have successfully implemented a combined ‘Marketplace + Retail Media’ strategy?

The marketplace opportunity for retailers

There are seven strategic reasons for retailers to adopt a marketplace model:

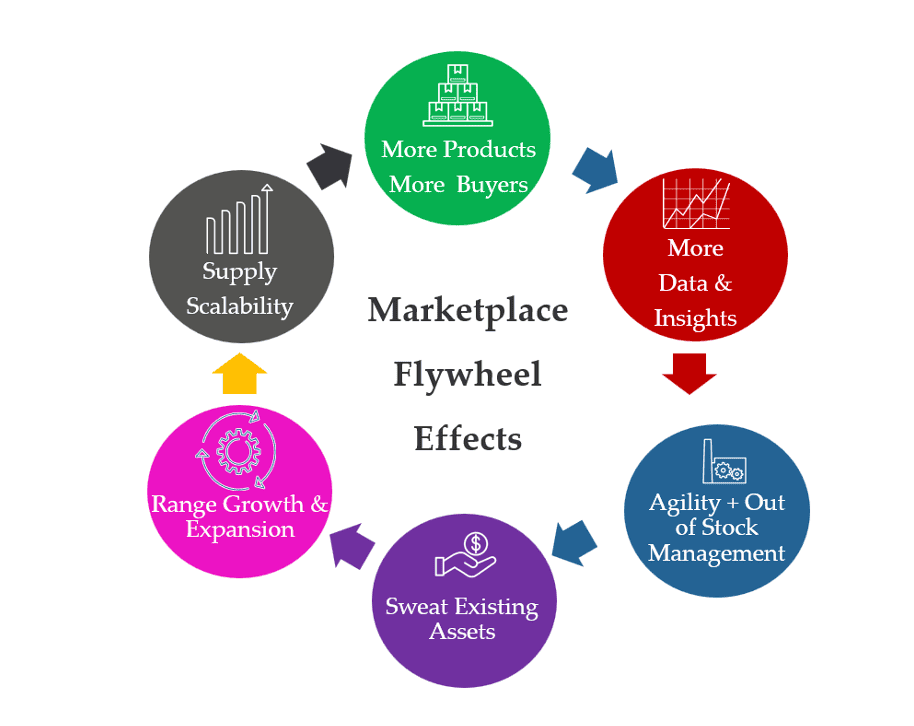

- Range growth and expansion: Retailers can improve their core offering with greater product depth and breadth, expanding into new categories and increasing cross-selling opportunities.

- Scalability of supply: Marketplaces do not require the same investment in direct sourcing as traditional models, providing efficiency when onboarding new sellers.

- Profit margins: Beyond the initial investment in technology and headcount, there are few large-scale CAPEX or operational set-up costs.

- Agility and out-of-stock management: Out-of-stock items lead to unhappy shoppers and missed sales. A curated marketplace ensures relevant third-party suppliers are available to ensure essential items remain in stock.

- Capture the long tail: SMBs and owner-operated businesses are often the source of innovation. While traditional buying teams would struggle to manage thousands of small suppliers, a marketplace captures this revenue without the manual investment required to curate and manage each account.

- Data enrichment: A wider range attracts more shoppers and generates more transactions. This leads to a wealth of first-party data, which directly increases the scale and value of the Retail Media opportunity.

- ‘Sweat existing assets’: Increasing the volume of products and listings improves the productivity of existing digital assets. This also boosts organic search visibility with Google and provides more “crawlable” content for LLMs like ChatGPT and Gemini.

Marketplace decisions for retailers

The strategic direction of a marketplace is defined by four fundamental decisions:

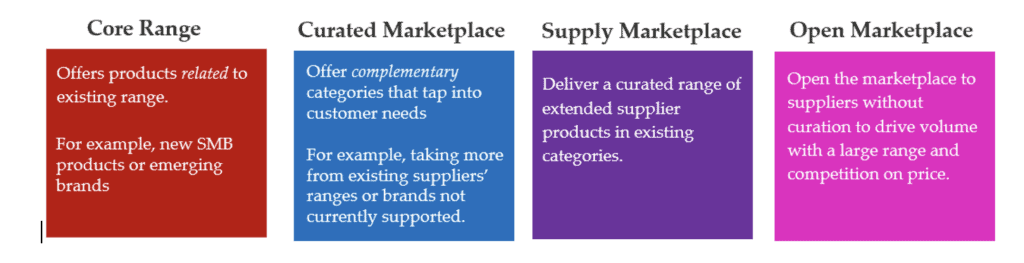

- The extent of curation: This is the most critical lever. Retailers must decide whether to strictly select suppliers that mirror their core range, curate specific adjacent categories, or adopt an “open” model. While an open model maximises scale, curation protects brand equity.

- Supplier onboarding and management: Operational efficiency is key. Retailers need to determine how they will vet, onboard, and manage thousands of third-party sellers without creating a massive administrative burden or “bottleneck” in the buying office.

- Growth vs cannibalisation: Retailers must weigh the benefits of new channel growth against the risk of cannibalising existing first-party (1P) sales. The goal is to ensure marketplace revenue is incremental and that the commission earned offsets any potential loss in direct sales margin.

- Control over customer experience (CX): There is an inverse relationship between scale and control. An open marketplace provides a vast selection but often requires the retailer to relinquish control over pricing, imagery, and content. The retailer must decide where they are willing to draw the line to maintain a premium shopping experience.

The choice of ‘core’, ‘curation’ or ‘open’ are business decisions that have ramifications for monetisation. Having an ‘open’ marketplace will mean a much bigger selection, and a much bigger opportunity for monetising all this extra data through Retail Media programmes.

However, opening the marketplace to all-comers could mean a degradation of the shopper experience and ultimately lower the monetisation opportunity in the long term.

Marketplace monetisation opportunities

Retailers have numerous ways to monetise a digital marketplace:

- Commissions: The most common stream, where the retailer takes a percentage (typically between 5% and 15%) of every third-party transaction.

- Subscription or listing fees: Charging sellers a monthly or annual membership fee or a listing fee to access the marketplace platform, often tiered based on the number of listings or level of support.

- Fulfilment & logistics services: Charging sellers to use the retailer’s existing warehouse and delivery infrastructure (like “Fulfilment by Amazon”), turning a cost centre into a revenue generator.

- Retail media: Selling ad placements like sponsored products, banners, and search to sellers.

While each of these streams is valuable, the most significant margin opportunity lies in retail media. A Retail Media Network (RMN) provides a substantial offset to the traditionally thin margins found in retail.

Retail media ad units like sponsored search typically deliver margins of 70% or more. By comparison, a typical grocery retailer operates on a margin of around 3%.

In other words, rather than relying solely on existing first-party traffic, a retailer can onboard an expanded roster of third-party suppliers. these sellers then utilise the Retail Media Network to ensure their products get visibility with the right shoppers.

As highlighted earlier, an increase in suppliers naturally leads to a broader product range. This expansion attracts more shoppers and drives more transactions, resulting in a vast increase in first-party data. This data is the engine of any Retail Media Network, allowing for the high-intent targeting that brands are willing to pay a premium for.

Case studies of retailers with digital marketplaces and Retail Media Networks

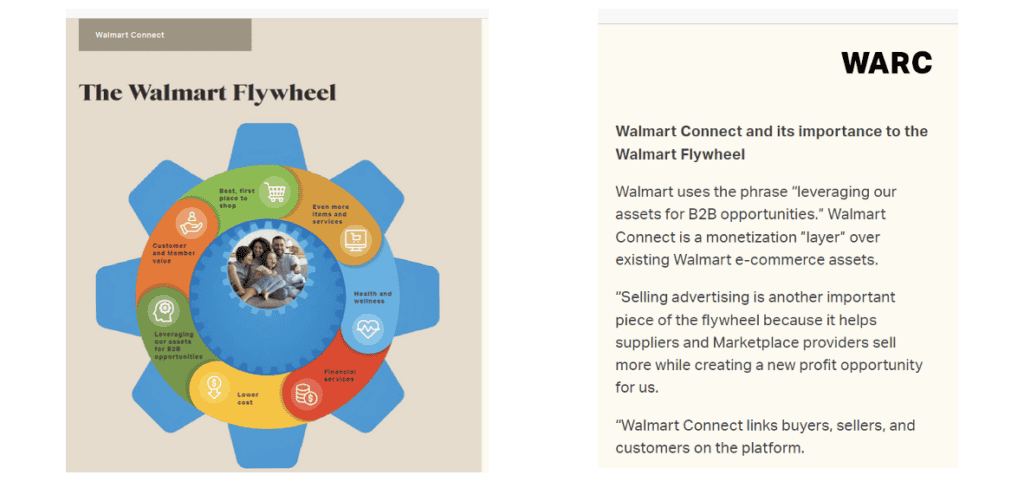

Walmart, US

Walmart are quite explicit about creating their own ‘Flywheel’ through their Retail Media business (called Walmart Connect) and the Walmart Marketplace.

What are the results of this strategy? Let’s hear directly from John Rainey, Walmart CFO and what he said about their strategy in 2025.

- “Global Walmart Connect advertising grew 27% to about $4.4 billion. Walmart U.S. Marketplace revenue grew 37%… The growth of this portfolio is expected to be one of the largest drivers of operating income growing faster than sales. These new profit streams allow us to expand our operating margins.”

- “We have the opportunity to grow general merchandise sales in stores with our first party e-commerce assortment and especially with our marketplace.”

- “U.S. e-commerce margins have significantly improved due to a shift in “business mix” (i.e., more ad revenue and marketplace fees) and lower delivery costs.”

- “We describe our business as being two P&Ls, a traditional store P&L, and the new digital P&L, with has got marketplace, membership, advertising. We think that the second P&L over time can be more profitable than the first P&L and lift the total.”

If you analyse the retail media business in Walmart, which is based on online, instore and the digital marketplace, every $1 earned through Walmart Connect is worth nearly $20 in retail sales in terms of profit impact.

Walmart is the biggest retailer in the world with stores and digital commerce businesses across the globe. What about country specific retailers without the scale of Walmart?

Let’s look at two markets that don’t get the ‘airtime’ about Retail Media and Digital Marketplaces, Portugal and France, and two retailers in particular, Worten and Rakuten.

Worten, Portugal: Creating a retail media and marketplace flywheel

Worten is Portugal’s leading electronics retailer. They have over 35% market share in core electronics categories, operate more than 200 stores, and maintain a formidable online presence through both eCommerce and the Worten Marketplace.

Portugal has a population of around 10 million, and while tourism and manufacturing are key industries, retail is deeply embedded in the national culture. Portuguese consumers value the physical shopping experience—touching products and shopping socially, particularly at weekends. Approximately 80% of the population uses mobile devices to discover brands and products. While the market is not yet as mature as the US or UK, Retail Media Networks are already gaining significant traction in grocery and electronics, where Worten competes alongside global giants like Amazon.

Inês Catão, Retail Media Director at Worten, joined from Google with extensive experience in advertising across multiple European markets. Her mission was to transform a traditional retailer with a strong digital footprint into a sophisticated advertising business with its own self-sustaining ‘flywheel’.

Catão explains: “Worten is quite unique in Portugal—and even in Europe—in that over 20% of our total sales happen online. In comparison, many large Portuguese retailers are closer to 8%. That makes our omnichannel model very compelling for consumers, brands and marketplace sellers.”

Several years ago, Worten made the strategic decision to treat Retail Media as a core media business rather than a commercial add-on. They recognised that a marketplace offered a major growth opportunity to democratise access and help smaller businesses scale online. Worten organises its Retail Media and Marketplace flywheel around two main pillars:

- Brands: Worten offers a full-funnel proposition, spanning awareness and consideration to performance and market share growth. Catão acknowledges that Worten Retail Media competes for budgets with TV, Google, Meta and TikTok, but points out: “Retail Media offers something those channels cannot: a closed ecosystem with deep insights into real consumer behaviour at the point of purchase.”

- Marketplace Sellers: Catão notes that “seller needs are different.” They prioritises fast results, simplicity and performance. Worten Retail Media offers advertising focused on consideration and conversion to help sellers gain visibility quickly. As these sellers mature, Worten introduces awareness formats, such as display and video, to support their next stage of growth.

Today, Worten hosts over 3,000 sellers on its marketplace, more than 50% of whom are international. For these sellers, the marketplace is an accessible gateway into the Portuguese market. In 2025, Worten began offering Retail Media solutions to these sellers, creating what Catão describes as a “win-win-win” model: sellers grow faster, customers receive better relevance, and Worten generates incremental revenue. To support this, Worten transitioned to using Mirakl for both its marketplace operations and its Retail Media Network.

The results

The impact of this strategic shift has been immediate:

- Advertiser Adoption: When Worten first introduced ads for marketplace sellers, fewer than 30 were investing. Following the shift to a more scalable technology platform, this grew to more than 350 active advertisers in just seven months.

- Revenue and Sales: Worten saw a 300% growth in monetisation revenue and a 40-point uplift in the sellers’ ability to generate sales.

- Efficiency: Marketplace-related Retail Media delivered an exceptional ROAS of 8.0 (800%), maintaining strong seller retention across a diverse range of categories.

Worten now plans to accelerate its digital marketplace expansion with the ambition to triple its 2025 results.

Rakuten, France: Retail Media, Marketplaces and BFCM

Rakuten France is one of Europe’s largest marketplaces, boasting fifteen million unique monthly visitors and a top-ten position in French digital commerce. The platform has a particular strength in high tech, household appliances and second-hand goods.

Kristina Raptovaia, Rakuten’s Head of Partnerships & Advertising / Retail Media, notes that Rakuten France positions itself as the destination with “always a coupon, always a promo, always a cashback offer. The brand promise is consistency: if you come on Black Friday, you will find what you are looking for at the best terms available on the internet.”

Black Friday Cyber Monday (BFCM) began as a US phenomenon but has evolved into a global shopping event – and France is no different. Raptovaia says: “There is a growing tendency in the French market to postpone major purchases to Black Friday. We see this year over year.”

Traditionally, BFCM is viewed as a sales spike that returns to the baseline immediately. However, promotional activity now begins much earlier, creating an overall lift to the baseline that often extends past Christmas into January. For Rakuten, November, December and January represent the strongest months in terms of traffic, GMV and committed Retail Media budgets.

The strategic challenges for the marketplace and retail media

Rakuten’s objective was to optimise the profitability of its Retail Media business, but they faced four recurring hurdles:

- Inventory Saturation: High-demand categories often hit capacity on-site during seasonal peaks like BFCM.

- Seller Scale: Traditionally, SMBs lacked the technical expertise and the budget scale to manage complex external accounts like Google Shopping.

- Conversion Intent: Most off-site extensions rely on display retargeting, which lacks the high conversion intent of on-site sponsored products.

- Operational Burden: Managing separate campaigns for on-site and off-site activation is time-consuming for smaller merchants.

The solution: automated orchestration

To address these, Rakuten created a unified solution using Mirakl Ads and Symbiosis. The strategy allowed every advertising euro to work hard, regardless of on-site inventory constraints:

- One budget, One setup: Advertisers create a single campaign that spans both on-site and off-site channels.

- Automated priority: The system prioritises on-site sponsored products (the most profitable channel). If on-site inventory becomes saturated, “leftover” budget is automatically redeployed to Google Shopping.

- High-intent off-site: By tapping into Google Shopping rather than standard display, Rakuten preserved the high ROAS that advertisers expect from search.

Kristina Raptovaia described the logic of this strategy for retail media:

“The large set of unmanaged suppliers need to be captured through self-serve platforms, not phone calls. The only way to reach them is through a seamless, self-serve interface. What we do off-site with Retail Media is allow our merchants to dynamically reallocate their total ad spend between on-site and off-site channels based on real-time performance. It is very fluid and simple: they see the results of their entire strategy in one interface.”

The results

The 2025 BFCM campaign delivered significant growth across the board:

- GMV growth: 15% increase versus the previous year (10% above projections).

- Retail media revenue: Increased by 20%, driven by the ability to capture budget that would otherwise have gone unspent due to inventory limits.

- Ad spend: On-site sponsored product spend increased by 40%.

- Efficiency: Off-site campaigns delivered a ROAS of 5.0, successfully capturing consumers at the awareness and consideration stages.

- Product winners: Sales were dominated by the iPhone 17 SE and AirPods, followed by air fryers and robot vacuum cleaners.

What’s next for Rakuten and retail media?

Raptovaia says “the main goal is to develop more formats and give access to 1st party data to attract new types of advertisers with display and video formats through Mirakl Ads. By offering new formats and access to first-party data, we should attract both long-tail and major brand advertisers, making them more visible to Rakuten’s audience.”

Retail media and marketplaces – the flywheel for revenue and growth: Five takeaways for Retail Media Networks:

- Build your own growth flywheel: For retailers operating a Retail Media Network (RMN), adding a marketplace creates a self-sustaining cycle. Marketplaces provide the scale (products and data), and retail media provides the margin (70%+ profitability). Combined, they are a proven driver of high-margin growth for retailers of all sizes.

- Scale is secondary to strategy: This model isn’t just for the Walmarts of the world. Whether you are a local leader like Worten or a country-specific leader like Rakuten, the mechanics remain the same.

- A fundamental mindset shift: Making marketplaces and retail media work requires a fundamental shift in how a retailer views its product range, its suppliers relationships and even the internal structure.

- Automation is the only way to capture the ‘long tail’: To scale retail media beyond your top 50 global brands, you must remove the friction of manual management

- Solve the inventory ceiling with off-site extensions: On-site inventory is a finite resource that hits saturation during peak periods like BFCM. By integrating off-site channels (like Google Shopping), Retail Media Networks prevent budget waste and capture a greater share of the advertiser’s total spend.